Biometric Payments: What Are They? How Secure is the Technology?

Biometric payment systems were not widely popular in The West until very recently. However, contactless payment technology has taken off in the US in the wake of the Covid-19 pandemic, and adoption doesn't appear to be slowing in the least. With new shopping channels and payment preferences comes the need for new verification methods.

The technology boasts some of the most advanced security features on the market today. It’s all but guaranteed to pull the rug from under traditional payment methods…at least once adoption reaches a critical mass, that is.

How can you take advantage of the many business benefits of biometric payment technology, without the hang ups? Let's talk about it.

Recommended reading

- What is EMV Bypass Cloning? Are Chip Cards Still Secure?

- Apple Pay: Fast, Secure, & Private… but is There a Catch?

- Terminal ID Number (TID): What is it? What Does it Do?

- The Top 10 Online Payment Processing Providers of 2024

- Is Open Banking Equipped to Fight Fraud?

- Google Pay: How to Sep Up & Accept Payments Using the App

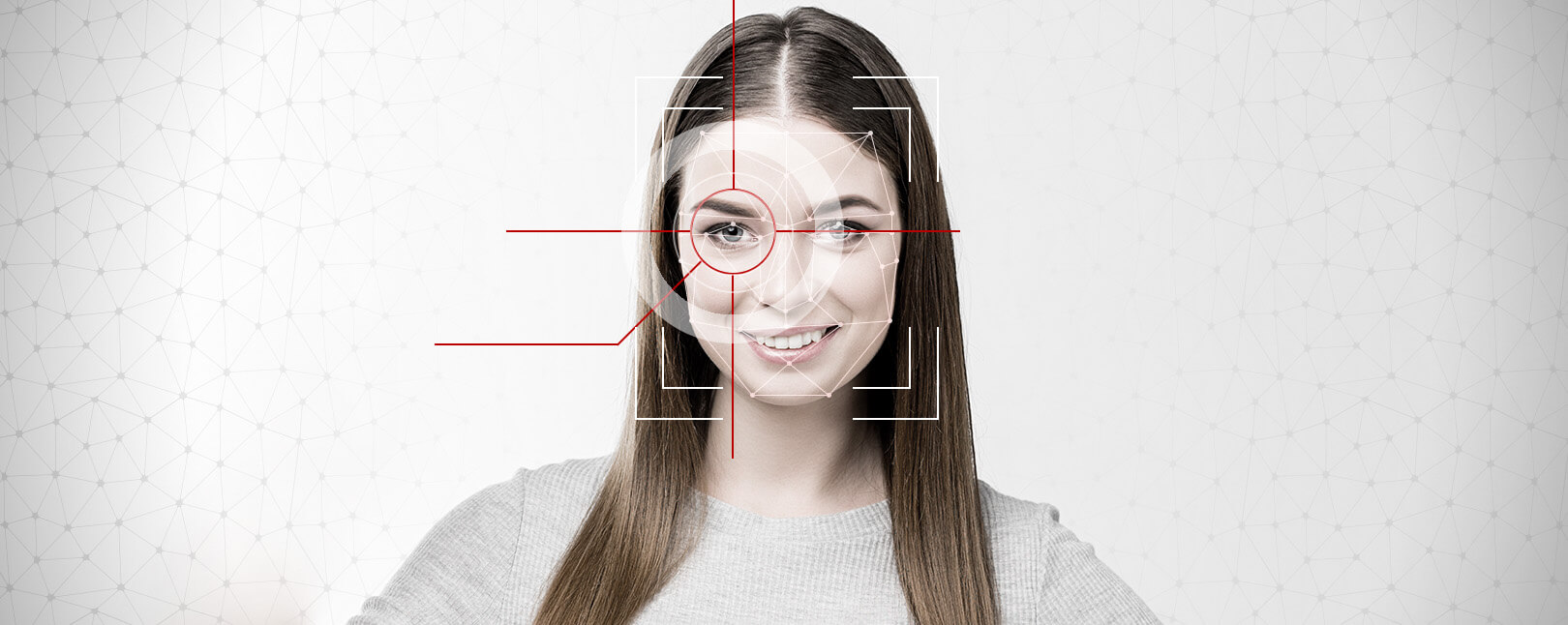

What is Biometric Authentication?

- Biometric Authentication

Biometric authentication is the practice of identifying individuals based on distinct physiological characteristics that are considered unique to each person. These can include fingerprints, facial recognition, DNA matching, iris recognition, heart rhythm, etc.

[noun]/* bī • ō • met • rik • ô • THen • ti • kā • SHən/

As the name implies, biometric security is a body of varied technologies, strategies, and practices that ensure security through biometric authentication.

Biometric security tools have countless potential applications. They can be used for anything from authorizing consumer payments to providing access to secured buildings. Biometrics can even help identify a suspect in a criminal investigation.

Biometric verification is, in general, much stronger and more reliable than other security techniques. Different technologies work by measuring different authentication factors, though. As a result, the effectiveness of using one specific indicator over another varies for different circumstances.

Electronic Payments: 3 Factors of Verification

To really understand the biometric payment system, we need to first examine this basic principle of electronic payment authentication. All methods of validating a user's identity in a transaction are based on one of three authentication factors:

Ownership is incredibly easy to spoof. For example, the security measure is broken if the physical card is stolen. Plus, anyone with the right know-how can use stolen cardholder information to counterfeit the card. It's even more accessible online where no card is present; the fraudster can simply use the cardholder's information by posing as a legitimate buyer.

Knowledge is also easy to bypass. Fraudsters are skilled at phishing attacks, card skimming, and camera manipulation to trick cardholders into surrendering sensitive information necessary to authorize purchases.

With alternate payments based on biometrics, though, you're employing inherence factors. These are more secure because the method of verification is physiological. After all, it's much harder to copy someone's fingerprint than to replicate a plastic card or a password.

How Do Biometric Payments Work?

- Biometric Payments

Biometric payments are transactions which employ biometric indicators like fingerprints, facial recognition, iris recognition, or heart rhythm to verify buyers’ identities during the transcription process.

[noun]/* bī • ō • met • rik • pā • məntz/

So, what biometric payment methods are currently available to authenticate eCommerce purchases? Below, we've compiled five of the most promising technologies for the payment space, and provided an overview of how they work:

New technologies present new opportunities...as well as new threats. Take steps to defend yourself today.

Ultimately, traditional payment card security is comparatively weak. Both the card-present and card-not-present environments relied exclusively on knowledge- and ownership-based authentication.

If a criminal had physical possession of a stolen card, there was a good chance the person could complete a fraudulent purchase. This would not be such an easy task with biometric technology in play, though.

The inherence factor makes it exponentially more challenging for criminals to spoof a user's identity. This gives biometric payments an edge over many potential fraud tactics.

Where are Biometric Payments Being Used Now?

The East Asian market (China, in particular) is where biometric payments first took off.

China's mobile payments adoption still leads the industry. Mobile payments technology has a total market penetration rate of nearly 41% in China; 44% higher than any other country in the world. Most of these transactions occurred via mobile payment apps like Alipay and WeChat.

Indeed, China seems to be shifting focus toward an entirely cashless economy. Using facial recognition technology in retail stores and fast food joints is swiftly becoming the norm nationwide. And, as the world's second-largest economy, the normalization of contactless payment methods was sure to inspire other markets.

In 2021, North America began to creep up on China's lead, with biometric payment cards taking point in 2022. Here are a few stats to illustrate this point:

- The global contactless payment market will see 9.5% compound annual growth through 2028.

- Global contactless payment volume will reach $56.565 billion by 2028.

- The majority of new payments hardware deployed in 2021 was biometric-enabled.

- More than 70% of Visa cards issued in New York supported biometric payments by April 2021.

Smartphone use among Western consumers produces broader familiarization with biometric technology. This is leading to wider acceptance of biometric payment cards. Also, consumers are demanding the technology more, as the biometric element is considered more secure.

This data suggests that biometric payments are expected to outpace all other payment methods globally in the next few years. The reasons for this are manifold, but besides boosted security, biometric payments pose an intriguing alternative to PIN and password security measures, which are increasingly hard to remember. Thus far, 86% of Americans and 7 in 10 Europeans are interested in the switch to biometric payments.

Advantages of Biometric Payments

Like we mentioned above, biometric payment technology is more advanced and secure than traditional ownership- or knowledge-based security. It’s considerably more difficult for fraudsters to access and replicate than previous security measures.

Beyond being more secure, biometric payment technology offers several other advantages as well. These include:

Common Objections to Biometrics

So, if biometric payments offer considerable benefits, why aren't they used in every transaction? Well, despite all the potential benefits of adopting biometric security, the technology still features several issues and weak points. You should be aware of a few drawbacks before you act:

A Broader Strategy is Required for Biometrics

Regardless of how extraordinarily advanced and forward-thinking biometric tech is and could still become, your business will need more than one method to fight fraud and chargebacks. At the same time, authentication methods must be accurate and efficient without causing friction at checkout.

Here are some tips you can take to introduce biometric payments into your practices. Follow these steps and you’ll be well on your way to an optimal anti-fraud strategy and a seamless customer experience:

Use More Than One Authentication Tool

No single tool can be 100% effective. Biometric security practices can still be defeated through several authentication spoofing tactics. Having a mix of multiple tactics can increase your odds of success.

You may have to experiment to find the right mix. Other fraud tools to consider include CVV verification, AVS, 3DS technology, geolocation, and fraud blacklisting, just to name a few.

#1 | Use the Most Comprehensive Data Available

The more data you can cross-reference, the more accurate you can be. Tap into the best data you can find, and use machine learning to constantly fine-tune results.

#2 | Keep Records Updated

Your authentication tools are only as good as the information you have on file. Perform regular account checks to update expired details held on-file.

#3 | Employ a Prevention Strategy

Biometric payment technology is a powerful fraud prevention tool, but it's only one tactic and affects only one fraud risk source. It won't help against chargebacks or first-party, post-transactional fraud. To fight back, you need a coordinated, carefully planned strategy to make the most of the tools at your disposal.

Conventional fraud detection tools have no impact on threats like friendly fraud. You'll need additional help to deal with this and other threats to your revenue.

Here at Chargebacks911®, we specialize in preventing post-transactional fraud that criminal fraud tools like those listed above can't reach. We work alongside other technologies to provide comprehensive, multilayered fraud defense. Continue below and get a free ROI analysis today.

FAQs

What is a biometric payment?

Biometric authentication is the practice of identifying individuals based on distinct physiological characteristics that are considered unique to each person. These can include fingerprints, facial recognition, DNA matching, iris recognition, heart rhythm, etc. Therefore, a Biometric Payment is an electronic payment made using this technology for verification

How do biometric payments work?

Biometric payments utilize inherence factors (something naturally or biologically inherent to the individual in question) to authenticate a user's identity and verify purchases. These payments are more secure because the verification method is physiological. After all, it's much harder to copy someone's fingerprint than to replicate a plastic card or a password.

What are examples of biometrics?

Biometric payment technology covers any technology that authenticates users through biometric means. This includes digital fingerprinting, facial recognition, voice recognition, iris scanning, and palm vein mapping, among others.

How safe is biometric security?

Biometric payments are more advanced and secure than traditional card-present and card-not-present transactions. It’s considerably more difficult for fraudsters to access and replicate or spoof biometric indicators than previous security measures.

Are biometrics required for a credit card purchase?

No, not as yet. That could conceivably change soon. 6 million contactless payment readers utilizing biometric authentication hardware are expected to ship by 2026. So, while you are not required to provide biometric authentication for credit card payments as yet, this is undoubtedly a “wait and see” situation.

Are there disadvantages of biometric systems?

Yes. Biometric payments are considered to be generally more secure than previous methods. However, there are a few potential downsides to consider, including availability, cost, privacy concerns, and other special circumstances (biological impairments, background noise, etc.).